— We take our content seriously. This article was written by a real person at BREL.

It’s October 17, 2016, and we are entering into brand territory in the Toronto real estate market: today, the recently announced changes to mortgage financing come into effect. Intended to cool down Canada’s red-hot real estate market, the changes will affect a number of Toronto Buyers and as a result, Toronto Sellers. If you haven’t been following the news, here’s a summary of the changes:

- Buyers with a downpayment of less than 20% (who are insured by CMHC) will have to qualify for a mortgage at a higher interest rate than the discounted rate. It doesn’t mean they’ll actually be paying that higher interest rate, but the banks want to be sure that buyers will still be able to afford their home if/when interest rates rise (they call this a stress test). For a Buyer approved for a purchase price of $930K in the Old World, they will now qualify to buy a property up to $775K in the New World. Most Buyers in this group will see their purchasing power reduced by 20-25%.

- The Good News: Long-term, we all benefit by people being able to pay their mortgages, if/when interest rates return to more normal levels. Non-CMHC insured mortgages (and thus most mortgages for properties priced over $1 million) are not currently impacted (though if you believe some rumours, banks might soon start stress testing all Buyers).

- The Bad News: Disproportionately, first-time Buyers will be impacted, and in a market as expensive as Toronto’s, that reduced purchasing power can make the difference between buying a house or not buying a house. Fewer Buyers, in theory, could mean a reduction in prices, which is not good for Sellers of course. That said, with supply and demand so completely out of whack in Toronto, we don’t anticipate huge price decreases; but the days of 20% annual increases are likely over (which let’s be honest, isn’t a bad thing).

- Other CMHC-insured mortgages (including those over $1 million) will also have to qualify at the higher interest rate. What you probably don’t know, is that banks sometimes buy insurance on your mortgage – even when you have a 20% downpayment. In those instances, they will have to qualify Buyers at the higher rate, which will reduce their purchasing power too. It’s not yet clear how many Buyers this will impact.

- You’ll now have to declare when you sell a property on your income taxes. For residents, the primary residence tax exemption still applies (which means that you won’t have to pay any capital gains tax on that home). But for non-residents, however, that exemption is gone.

Follow Us!

Stay tuned to the BREL blog as we continue to share what we’re seeing and feeling down here in the trenches. Toronto has proven itself resilient to changes meant to decelerate our market in the past, and while this might just be a blip in history, this could also be the beginning of a few tumultuous months.

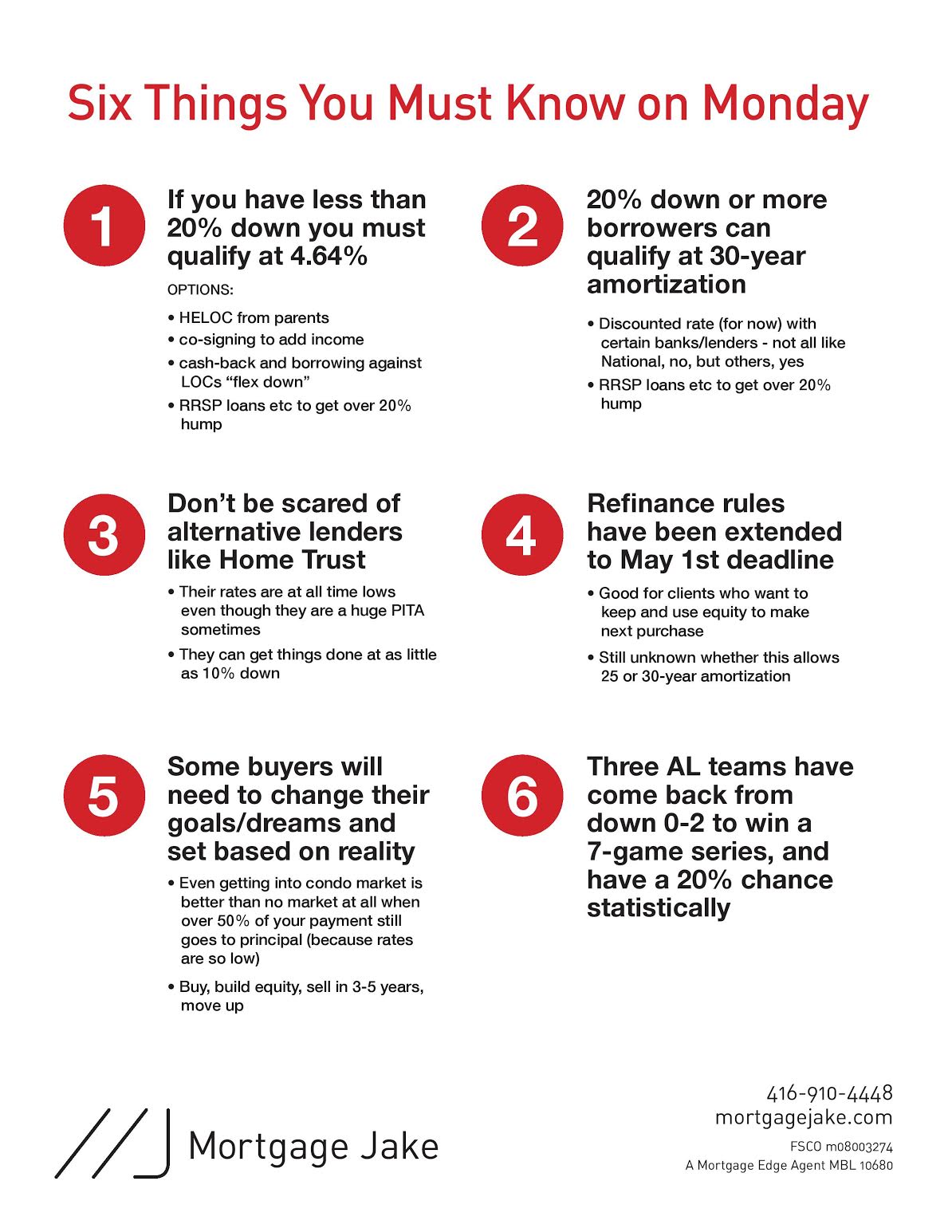

See What Mortgage Jake Wants You to Know

Jackie Hayden says:

Its also important to understand that ALL Banks will be able to finance low down payment clients at 4.64% as before, and that clients who are already FIRM approved at their lender have no impact to these changes. The important thing to remember is that clients who are FIRM approved by a lender such as RBC, have their appraisal, credit check and income check already completed,and have nothing to worry about. We think these changes are minimal as they affect only those who were not approved by CMHC prior to the announcement. Please check with your lender. Its critical to ensure that your approval is sound. Our Firm Approval is differentiated in that we pull a credit bureau up front, and ensue all income and down payment is verified. That provides you with peace of mind as the financing condition is truly met at RBC!