— We take our content seriously. This article was written by a real person at BREL.

In a world where less can often mean more, downsizing your home can be a savvy financial move that can transform your life. Whether you’re an empty nester, a retiree looking to cut costs, or simply seeking a more minimalist lifestyle, downsizing can unlock so many savings. In this guide, we’ll explore how downsizing your home can save you money and provide you with tips and strategies to make the transition smooth and rewarding.

1. Smaller Property, Smaller Price

One of the most obvious benefits of downsizing is the savings you’ll reap from having a smaller mortgage – or maybe no mortgage at all! When you opt for a smaller property, whether it’s a smaller house or a condo, you’ll free-up cash to redirect towards other financial goals or investments.

Tips & Strategies:

If your goal is to lower your overall housing costs, make sure to maximize the size of your downpayment on the new home – avoid the temptation to only provide the minimum downpayment. If you can, maintain your current amortization (the total length of your mortgage) vs. starting over with a new 25-year mortgage. If you have 18 years remaining on your mortgage, work with your lender to keep your new mortgage amortization to 18 years – or shorten it if you can, to save on lifetime interest costs. Don’t forget to shop for the best interest rate!

2. Lower Utility Costs

A smaller home typically means lower utility costs. Reduced square footage means less space to heat, cool, and light. You’ll notice the difference in your monthly utility bills, leaving you with extra money in your pocket.

Tips & Strategies:

There are other ways to lower your utility costs. Opt for energy-efficient appliances and lighting and use a smart thermostat to regulate heating and cooling. We wrote about ways to lower your costs by focusing on saving energy here.

3. Declutter and Sell Some Stuff

Downsizing forces you to declutter and evaluate your possessions. You’ll likely find items you no longer need or use. Selling these belongings can put extra cash in your pocket or be used to offset moving expenses.

Tips & Strategies:

You might be surprised at how much money you’ll be able to generate by selling some of your not-used or not-really-loved possessions – and you might even be able to get a tax receipt for donations. We wrote a blog with detailed strategies about downsizing your personal belongings here.

4. Lower Maintenance Costs (Especially in a Condo)

If you’re downsizing to a condo, you’ll appreciate the reduced maintenance costs. Condo associations cover major repairs and maintenance from the monthly fees you pay. This greatly reduces the need for a financial buffer for unexpected home repairs.

If you’re moving from a bigger to a smaller house, you’ll still see maintenance savings from reduced interior square footage and a smaller yard.

Tips & Strategies:

There are so many ways to reduce your maintenance costs! We wrote a whole blog about saving money on home maintenance here.

5. Lower Property Taxes

In Ontario, homes are taxed at their assessed value, which is determined by MPAC every 4 years. The lower your assessed value, the lower your property taxes. For example, if your current home is assessed at $1.6 million, your property taxes are $10,660 in 2023. If you move to a home assessed at $1 million, your property taxes would reduce to $6,662 a year.

Tips & Strategies:

Click here to calculate estimated property taxes on a home in Toronto.

6. Lower Insurance Costs

Smaller homes generally come with lower insurance premiums. Reduced square footage means less to insure, leading to savings on homeowners’ insurance.

Tips & Strategies:

Don’t make the mistake of under-insuring your home – those savings aren’t worth the risk if you have a fire or flood. Insurance is there to protect you in the event of catastrophic loss. To save money on home insurance, compare quotes from different providers, bundle your home insurance with your car insurance and talk to your insurance company about other options like increasing the size of your deductible.

7. If You Have To, Refinance Existing Debt at the Same Time

When you downsize, it’s an opportunity to evaluate your existing debts and see if you can save any money on interest costs. Consider refinancing high-interest loans or credit card debt by rolling them into your new mortgage to reduce monthly payments and interest.

Tips & Strategies:

Your home is not a bank machine and when you roll debt into a mortgage or home equity line of credit, you reduce the equity in your home and increasethe amount of interest you pay over time. Consult with your financial advisor to assess your debt situation and explore refinancing options.

8. Less Room For Stuff = Less Stuff

A smaller home naturally limits the space available for storing possessions, meaning you’ll be more mindful of what you buy, leading to fewer expenses.

Tips & Strategies:

Adopt a “one in, one out” rule for new purchases to maintain clutter-free living. Embrace minimalism and focus on buying items that truly add value to your life.

9. Don’t Pay for Rooms You Don’t Use

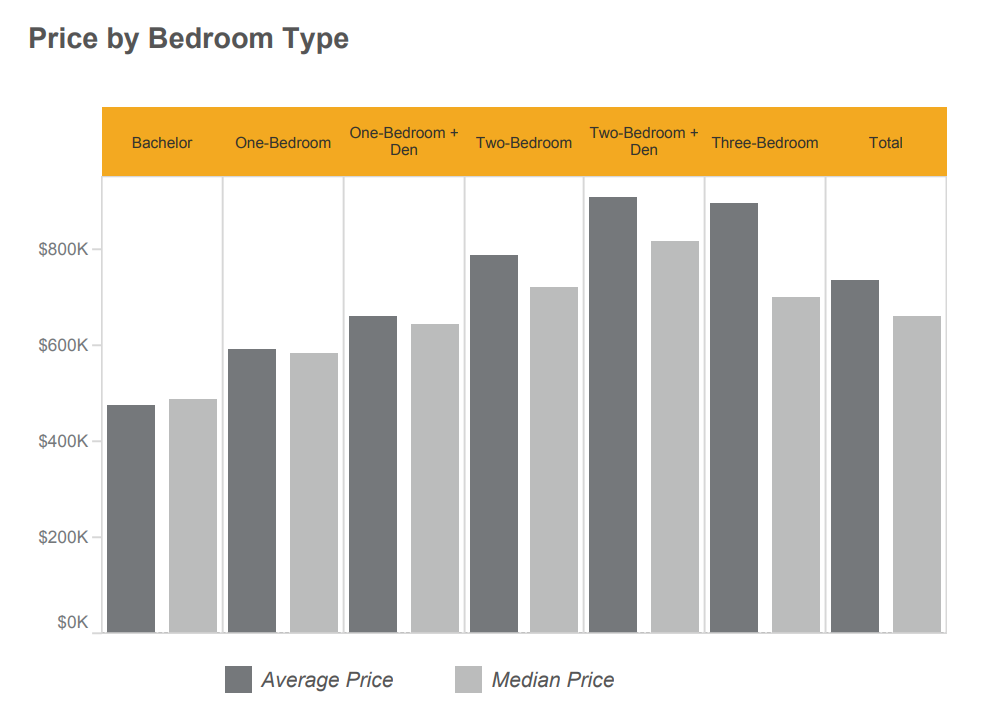

One of the often-overlooked benefits of downsizing is the savings you get from not paying for space you don’t use. If you currently have rooms in your home that you don’t regularly use – I’m looking at you, formal dining room and spare bedroom – downsizing to a smaller space can eliminate those extra expenses.

If you currently live in a 2-bedroom condo and only have guests use the spare room a few times a year, it might make financial sense to downsize to a one-bedroom condo. Here are the average prices for a condo in the GTA, by number of bedrooms, in Q2 2023.

Tips & Strategies:

Assess your lifestyle and prioritize the spaces you truly need in your new home. Allocate the extra funds towards experiences or activities that enrich your life.

10. Explore Shared Living Space

If you’re open to more radical downsizing, consider co-living or shared housing arrangements. These options often come with lower living costs, communal amenities, and a sense of community.

Tips & Strategies:

Research shared housing opportunities in your area. Ensure compatibility with potential housemates before committing to having someone move into your home.

11. Invest the Savings

Don’t forget to put your downsizing savings to work! Talk to your financial planner to help you diversify and maximize your investments.

Saving money is one of the number ones people choose to downsize. Be smart, be strategic and reap the rewards.